Unearned revenue

The most basic example of unearned revenue is that of a magazine subscription. When we register for unearned revenue an annual subscription of our favorite magazine, the revenue received by the company is unearned.

Unearned revenue on the other hand is that which has been received but not yet earned (worked for). We received a lot of unearned revenue , but knew we would be getting accounting equation paid really soon, due to pour track record. This journal entry reflects the fact that the business has an influx of cash but that cash has been earned on credit.

When the goods or services are provided, this account balance is decreased and a revenue account is increased. To learn more, see Explanation of Adjusting Entries. The revenue recognition principle dictates the process and timing by which revenue is recorded and recognized as an item in a company’s financial statements. Theoretically, there are multiple points in time at which revenue could be recognized by companies.

Unearned Revenue Journal Entries

The rationale behind this is that despite the company receiving payment from a customer, it still owes the delivery of a product or service. If the company fails to deliver the promised product or service or a customer cancels the order, the company will owe the money paid by the customer. If a publishing company accepts $1,200 for a one-year subscription, the amount is recorded as an increase in cash and an increase in unearned revenue.

Companies prefer unearned revenues in the form of cash because this way, they can be sure that the buyer is committed to purchasing goods or services from them. Thus, when unearned revenues are recorded the cash account under the assets is unearned revenue debited, and the unearned revenues account under liabilities is also increased. In accrual accounting, revenue recognition can become complicated, especially when companies sell subscription services or complete projects in installments.

Unearned revenue is recorded on a company’s balance sheet as a liability. Unearned revenue, also known as deferred revenue, is income received by a business for work not yet https://www.bookstime.com/ done. It is an advance payment for work expected to be done at a later date or time. Once the business actually provides the goods or services, an adjusting entry is made.

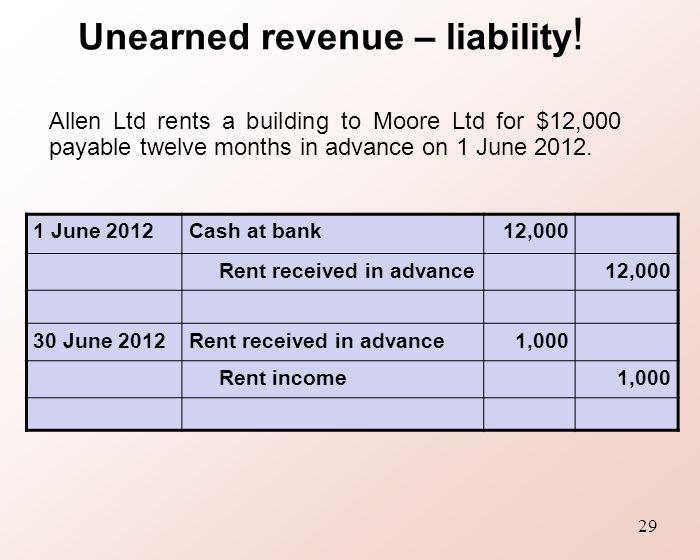

When a check for the full years rent is received, it creates a problem; the income has not yet been earned. Therefore rent is unearned income and must be treated as a liability until we earn it.

Since theGAAP requires to record the sale transaction when it occurred, the airline companycannot register this income as revenue yet. Thus, it is filed under liabilities on thebalance sheet in the Unearned Revenues account. Since the payment is expectedwithin the same reporting period, the transaction would fall under short-term liabilities. Since the company owes gods or services to the customers, the unearned revenues areconsidered liabilities. In most cases, the deferred revenues are classified as short-termliabilities because the obligations are typically fulfilled within less than a year.

- Only when the company has fulfilled itsobligation — earned money — is the liability removed and the money is recorded asrevenue and included in the income statement.

- The line item “Unearned Revenue” or “Deferred Income” gives the company a place to recognize that the cash payment has come in but the company has deferred the revenue recognition until a later date.

- Because there is a possibility that the services may not be performed (whether because a customer backs out or a business is unable to perform them) they present a risk to the company.

- Unearned revenue is a current liability and is commonly found on the balance sheet of companies belonging to many industries.

There are two ways to report unearned revenue – a liability method andan income method. Suppose on March 15, 2015, Example Company received a$24,000 advance payment for the maintenance services it will provide during half of thismonth and in the following month. Lets’ review how one transaction will have differentjournal entrees depending on which method is used.

ABC is in the business of publishing Business Magazine. The company receives an Annual subscription of Rs 12000 from one of its clients on 31.03.2018 for the next year. Revenue will be earned when the magazine will be delivered management accounting to the client on a monthly basis. Unearned Revenue Balance Sheet as on 31.03.2018 will show an increase in Cash Balance by the amount of Annual subscription of Rs 12000 and Unearned Income, a liability, will be created.

Well, the short answer is that both terms mean the same thing — that a business has been paid for goods or services it hasn’t provided yet. Here’s a more thorough description of deferred and unearned revenue, as well as a few examples to illustrate it. The seller recognizes “unearned revenues” (or “deferred revenues”) as revenues received for goods and services not yet delivered. To balance the accounting records, the bookkeeper will also make a record in the Cashaccount under assets. The transaction will increase both the Cash and UnearnedRevenue accounts.

Public companies and almost all large firms nevertheless choose double entry and accrual accounting. They do so because it is nearly impossible for them to meet government reporting and record-keeping requirements using a single-entry system alone. And, they choose this approach because it enables them to track manage revenues and expenses, as well as liabilities, owners equities, and assets. By contrast, Single entry accounting serves only for managing cash outflows and inflows.

What are some examples of deferred revenue becoming earned revenue?

The money shows up as a liability on the balance sheet, because the company has possession of money that it hasn’t earned. Unearned revenues occur when companies follow the accrual basis of accounting. When advance payments are received for products or services that will be delivered or completed in the future, the earnings process is not complete.

The business has not yet performed the service or sent the products paid for. Unearned revenue is reported on a business’s balance sheet, an important financial statement usually generated with accounting software. Unearned Sales Revenue results in cash exchange before revenue recognition for the business. However, if a business does not follow the correct accrual method of recognition of Deferred Revenue it can overstate the revenue and resultant profitability without recognizing the corresponding expenses to generate such revenue.

For example, a company receives an annual software license fee paid out by a customer upfront on January 1. However, the company’s fiscal year ends on May 31. So, the company using accrual accounting adds only five months’ worth (5/12) of the fee to its revenues in profit and loss for the fiscal year the fee was received.